Every spring, a familiar question begins to circulate among my clients, at dinner tables, in open house lineups, and in the messages I receive on quiet Sunday mornings.

"Do you think rates are going to go up or down?"

It is one of the most human questions in real estate. We all want to know what is coming. We want to time things well. We want to feel confident that the decision we are about to make is the right one.

The honest answer, of course, is that nobody knows for certain. Not me, not your bank, not the Bank of Canada itself. But what we do have — and what is genuinely useful — is a window into what Canada's most sophisticated financial institutions are currently forecasting. And right now, that window reveals something worth paying close attention to.

Where Rates Stand Today

Before we look ahead, let us anchor ourselves in the present.

The Bank of Canada's overnight rate currently sits at 2.25%, following four consecutive meetings with no change. The prime rate — the benchmark most lenders use to set variable mortgage rates — is 4.45%. These numbers are the foundation upon which every mortgage conversation in Canada is currently being built.

For context, the overnight rate peaked at 5.00% in 2023 and 2024, before the Bank began cutting. It has come down significantly since then — a journey that brought real relief to variable-rate mortgage holders and renewed energy to buyers who had been waiting on the sidelines.

But now the cutting cycle appears to have paused. And the question everyone is asking is: what happens next?

Why Forecasting Matters More Than Ever

In a stable, predictable rate environment, bank forecasts are helpful but not urgent. When rates are moving slowly and consistently in one direction, most borrowers can plan with reasonable confidence.

But we are not in a stable, predictable environment right now.

We are navigating a landscape shaped by Middle East conflict and oil price shocks, ongoing Canada-US trade tensions under CUSMA negotiations, a Canadian economy growing at near-zero in March 2026, rising mortgage arrears reaching their highest point in over a decade in Ontario, and bond market volatility that saw the 5-year yield swing by 0.64% in less than a year.

In this environment, the gap between the most optimistic and most cautious bank forecasts tells its own story. And that story deserves to be read carefully.

What Each of Canada's Big 6 Banks Is Currently Projecting

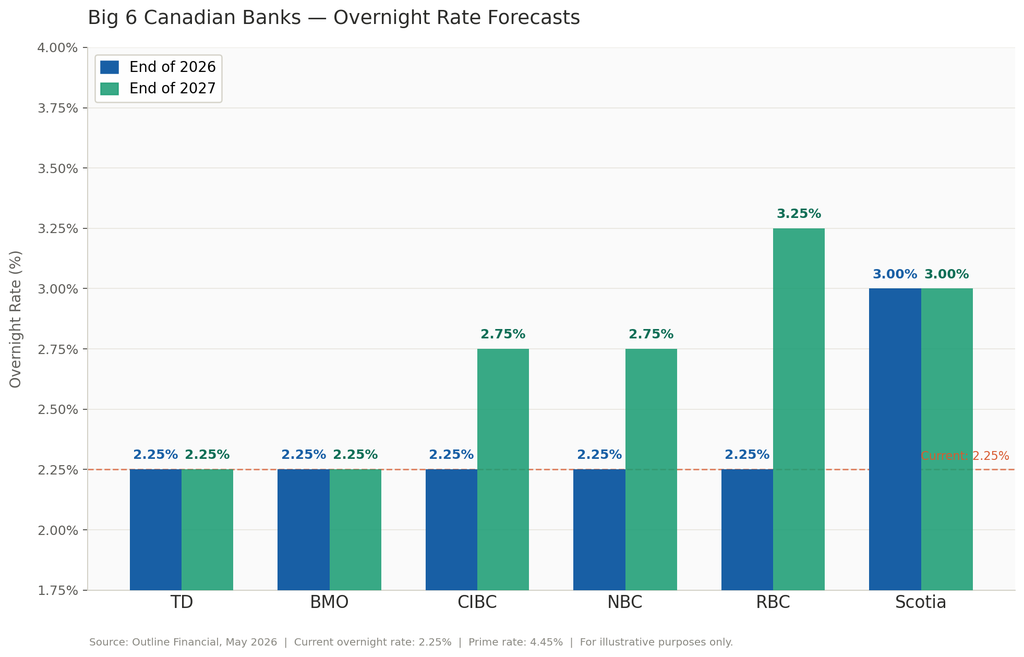

These forecasts were compiled from each bank's publicly available research as of early May 2026. They represent the overnight rate — the Bank of Canada's policy rate — not mortgage rates directly.

TD Bank is projecting that the overnight rate will remain at 2.25% through the end of 2026, and stay there through the end of 2027 as well. TD's view is one of extended stability — that the current rate is broadly appropriate given the economic backdrop, and that significant movement in either direction is unlikely in the near term.

BMO shares a very similar outlook to TD, forecasting the overnight rate holds at 2.25% through end of 2026, with rates remaining flat or only modestly higher by end of 2027 at approximately 2.25%. BMO's stance reflects a belief that the economy needs continued support and that inflationary pressures, while present, are not severe enough to warrant tightening.

CIBC projects the overnight rate will remain at 2.25% through the end of 2026, with a modest increase to approximately 2.75% by the end of 2027. CIBC's forecast acknowledges the possibility of upward pressure over the medium term, while stopping well short of predicting aggressive hikes.

NBC (National Bank of Canada) aligns closely with CIBC, projecting the rate holds at 2.25% through 2026, rising gradually to around 2.75% by end of 2027. NBC's research team has consistently highlighted the fragility of Canadian consumer spending and the labour market as factors that would limit the Bank of Canada's appetite for rate increases.

RBC takes a slightly more hawkish view over the longer term. While projecting stability at 2.25% through end of 2026, RBC forecasts the overnight rate climbing to 3.25% by end of 2027 — the highest projection among the major banks for that time horizon. This would translate to a prime rate of approximately 5.45%, meaningfully higher than today's 4.45%.

Scotia Bank stands as the clear outlier in the near term. Scotia is projecting the overnight rate will rise to 3.00% by the end of 2026 — a full 0.75% above where it sits today. By end of 2027, Scotia maintains that 3.00% forecast. Scotia's research team has placed greater weight on energy price inflation, the potential for tariff-driven price pressures, and what they see as a tighter labour market than the consensus view suggests.

Reading Between the Lines

What do these forecasts tell us collectively? A few things stand out.

First, the majority of Canada's major banks believe rates will hold relatively steady through 2026. That is a reassuring baseline. It suggests that for most borrowers, the immediate environment is unlikely to become dramatically more expensive in the short term.

Second, the longer-term picture is considerably less certain. By end of 2027, forecasts range from 2.25% all the way to 3.25% — a full percentage point of difference. On a $600,000 mortgage, that difference translates to roughly $350 to $400 more per month. Over a five-year term, that is approximately $21,000 to $24,000 in additional interest costs. That is not a small number.

Third, Scotia Bank's outlier position deserves respect, even if the consensus sits lower. Scotia has consistently been among the more data-driven forecasters in Canada, and their emphasis on energy-driven inflation is not without merit. The Bank of Canada itself acknowledged in its most recent Monetary Policy Report that if oil prices remain elevated, consecutive rate hikes could be necessary.

Finally, bond markets are already pricing in meaningful near-term uncertainty. As of early May 2026, there was approximately a 44% probability of a rate hike at the June 10th Bank of Canada meeting — up dramatically from just weeks prior. Fixed mortgage rates, which follow bond yields rather than the overnight rate directly, have already been moving in response. The 5-year bond yield reached a peak of 3.26% on April 29th — its highest point in the recent cycle.

Reading Between the Lines

What do these forecasts tell us collectively? A few things stand out.

First, the majority of Canada's major banks believe rates will hold relatively steady through 2026. That is a reassuring baseline. It suggests that for most borrowers, the immediate environment is unlikely to become dramatically more expensive in the short term.

Second, the longer-term picture is considerably less certain. By end of 2027, forecasts range from 2.25% all the way to 3.25% — a full percentage point of difference. On a $600,000 mortgage, that difference translates to roughly $350 to $400 more per month. Over a five-year term, that is approximately $21,000 to $24,000 in additional interest costs. That is not a small number.

Third, Scotia Bank's outlier position deserves respect, even if the consensus sits lower. Scotia has consistently been among the more data-driven forecasters in Canada, and their emphasis on energy-driven inflation is not without merit. The Bank of Canada itself acknowledged in its most recent Monetary Policy Report that if oil prices remain elevated, consecutive rate hikes could be necessary.

Finally, bond markets are already pricing in meaningful near-term uncertainty. As of early May 2026, there was approximately a 44% probability of a rate hike at the June 10th Bank of Canada meeting — up dramatically from just weeks prior. Fixed mortgage rates, which follow bond yields rather than the overnight rate directly, have already been moving in response. The 5-year bond yield reached a peak of 3.26% on April 29th — its highest point in the recent cycle.

What This Means for Buyers, Sellers, and Homeowners

If you are a buyer currently in the market or preparing to enter it, the message from these forecasts is nuanced but actionable. Most banks do not expect dramatic rate increases in the near term, which means the current mortgage rate environment remains relatively accessible compared to the peak years of 2023 and 2024. A TRREB condo apartment that would have cost approximately $3,110 per month in March 2024 costs roughly $2,414 per month today — a meaningful improvement in affordability driven by both lower prices and lower rates.

At the same time, the upside risk is real and growing. Locking in a rate hold now — typically valid for 90 to 120 days — costs you nothing and protects you from a potential increase before your closing date.

If you are a homeowner approaching renewal, understanding this forecast range helps you make a more informed decision between fixed and variable. A variable rate benefits you if rates stay flat or fall. A fixed rate protects you if Scotia Bank or RBC's higher-end projections prove correct. The right choice depends on your personal financial situation, your risk tolerance, and your timeline — and it is worth having a thoughtful conversation with a trusted mortgage professional before you decide.

If you are a seller, these forecasts carry a different kind of relevance. Buyer affordability and confidence are closely tied to rate expectations. A stable or improving rate environment supports demand. An unexpected rate hike — particularly if it catches the market off guard — can soften activity quickly, as we have seen before.

The Bigger Picture

Forecasts are not guarantees. Every bank on this list has been wrong before, and they will be wrong again. The world in 2026 is moving faster and less predictably than most economic models are designed to handle.

But forecasts are not meant to be perfect. They are meant to be useful. They give us a framework for decision-making, a sense of the range of possible outcomes, and a reminder that preparation — not prediction — is the foundation of sound real estate planning.

The clients I serve who navigate market uncertainty best are not the ones who waited for perfect clarity. They are the ones who got informed early, built a plan that could weather different outcomes, and moved forward with confidence rather than fear.

That is what I am here for. Whether you are weighing your first purchase, your next move, or a long-term investment strategy, I would love to sit down with you and talk through what these forecasts mean for your specific situation. I am also happy to connect you with a trusted mortgage partner who can help you explore your options in detail.

Real estate is not just about the market. It is about your life, your goals, and your future. And with the right guidance, even uncertain times can lead to extraordinary outcomes.

With you beyond the transaction — always.

Check out this article next